Proud Member of the Rapid Response Team for:

![]()

Click Here To Learn More About How You Can Help

Or

Call 412-378-8779

Categories

- 2012

- 2013

- 2016

- 2017

- 2018

- Advertising

- Advocacy

- Amazing!

- Appellate Practice

- Apps for Lawyers and Others

- AVVO Answers

- Bankruptcy

- Blawging

- Business

- Casa San Jose

- Case Update

- Christmas!

- Civil Litigation

- Civil Rights

- Civility and Courtesy in the Practice of Law.

- Congressional Redistricting

- Constitutional Law

- Construction Law

- Consumer Protection

- Contract Law

- Coronavirus

- Courthouse Scenes

- COVID-19

- Credit Card Collection Litigation

- Criminal Law

- Cyber security

- Decision making

- Employment Law

- Encore Post

- Environmental Law

- Estates and Trusts

- Ethics

- Evidence

- Fair Housing

- Fake News

- Family Law

- Fifty Years Ago

- fracking

- Future of the Law

- Great Lawyers

- History

- Holidays

- How to . . .

- Humor and Satire

- Immigration

- insurance

- Jack Sez

- Landlord and Tenant law and litigation

- Lawyering

- Legal Education

- Legal Ethics

- Legal History

- Legal Marketing

- Legal Technology

- Legal Writing

- Life Affirmation

- Life on the Internet

- Links

- Milestones

- Mortgage Foreclosure

- News Commentary

- Oil and Gas

- On line chicanery

- On-line Security

- One Hundred Years Ago

- Oriegate

- Orphan's Court Practice

- Personal Privacy

- Personal Productivity

- Phishing

- Pittsburgh

- Pittsburgh Legal Back Talk

- Pittsburgh Legal Community

- Pokemon Litigation

- Politics and Government

- Post September 11

- Practice of Law

- Privacy

- Property Assessments

- Real Estate

- Real Estate Contracts

- Reassessment 2012

- Retweets

- Right to Reputation

- SCOTUS

- Screenshots!

- Security and Privacy

- Senior Lawyers

- Seven Foundations of Time Mastery for Attorneys

- Signs of the Times

- Solo by Choice: The Review

- Tell Us Something . . .

- Ten Years of Pittsburgh Legal Back Talk

- Tenth Anniversary

- Tenth Anniversary Year of PLBT

- The continuing American Revolution

- the Review

- trademark and service mark

- Trends in the Law

- UTPCPL

- Vocabulary Word of the Day

- Weekend Book Review

- Winners and Losers

- Words Lawyers Use

- Workers Compensation

- Zoning

Real Estate and Consumer Protection: Consumer Financial Protection Bureau Is Attempting To Simplify Loan Disclosures.

Posted By Cliff Tuttle | September 24, 2011

No. 719

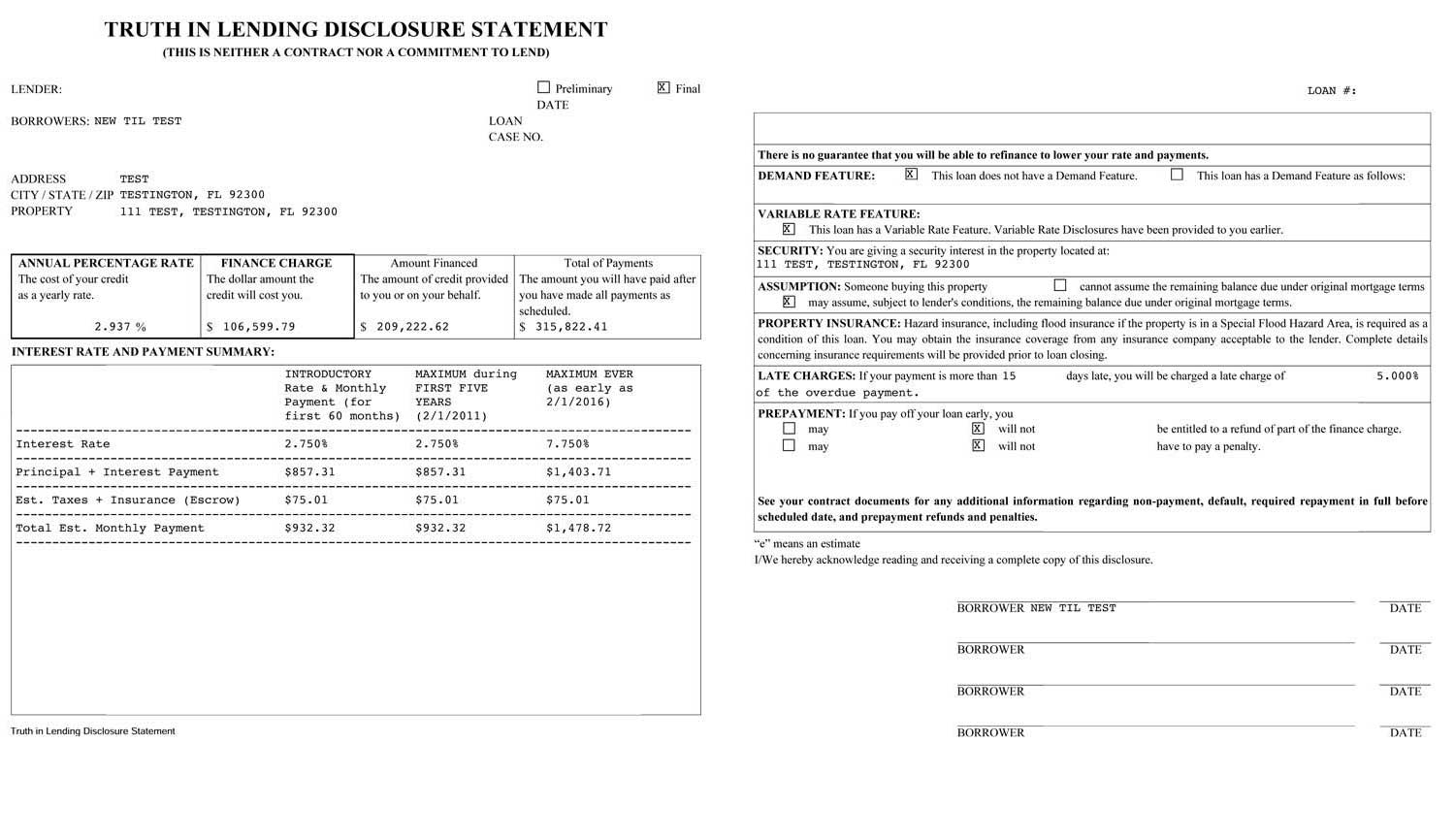

The Consumer Financial Protection Bureau, which was created by the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, has been quietly experimenting with combining the two major home mortgage disclosure documents, the Truth in Lending Disclosure (TIL) and the Good Faith Estimate (GFE).

The Consumer Financial Protection Bureau, which was created by the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, has been quietly experimenting with combining the two major home mortgage disclosure documents, the Truth in Lending Disclosure (TIL) and the Good Faith Estimate (GFE).

They developed a couple of versions of new disclosures, which look like this or this. After creating a form based upon feedback from consumers (both by email and at field project sites) they asked recipients to read two disclosures using that form and tell them which of two hypothetical loans was the better deal.

If you clicked on the disclosures above, you may have noticed that the familiar four boxes on the top of the Truth in Lending disclosure are not there. These disclosures have baffled consumers for a couple of generations. The APR typically scares them (but only for a minute or two) into thinking that the interest rate has been stealthily increased. Upon receiving an explanation, even if it hardly made sense, they returned to calm. The other numbers, the Finance Charge, the Amount Financed and the Total of Payments also caused temporary disquiet. But the borrowers, who typically went through this process once in a decade or two, didn’t have the experience to evaluate these numbers. All of them looked astronomically high. So in the end, the borrowers almost always took the deal, regardless of what the disclosures said. The experimental forms still contain comparison information, but it is downgraded in importance and explained better. As useful as the experimental form may be, however, it can’t force a consumer to read it, think about it or ask questions. Most of us just don’t read disclosures, no matter how well-designed. That’s just the way it is.

The truth was and is that government-mandated disclosures, no matter how graphically displayed, are not capable of educating the borrower sufficiently to walk away from a bad deal. But this failure was not with disclosure, it was with underwriting. For generations, home lending was governed by regulations written to insure that the borrowers would be able to afford the payments. The creativity of brokers, who were subject to much less regulation, bent and then broke a system that had worked fairly well.

Disclosures did not prevent borrowers from making bad decisions — and they probably never will — but they do protect the brokers. How, after all, can you complain after the fact about something that was fully disclosed? How indeed.

In the bad old days, loan originators frequently sold consumers loans with terms that that were far from the best available to them. The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 and the Consumer Financial Protection Bureau are attempting to end these practices. Considering history, it is clear that the subject cannot be simply left to government agencies, no matter how well-intentioned. This stuff is important and it is vital to everyone that we get it right this time.

We’ll examine those efforts and follow future developments in this blog.

CLT

Welcome

CLIFF TUTTLE has been a Pennsylvania lawyer for over 45 years and (inter alia) is a real estate litigator and legal writer. The posts in this blog are intended to provide general information about legal topics of interest to lawyers and consumers with a Pittsburgh and Western Pennsylvania focus. However, this information does not constitute legal advice and there is no lawyer-client relationship created when you read this blog. You are encouraged to leave comments but be aware that posted comments can be read by others. If you wish to contact me in privacy, please use the Contact Form located immediately below this message. I will reply promptly and in strict confidence.

Recent Posts

- Sheriff Sales in the COVID-19 Era

- MORTGAGE FORECLOSURE: Cares Act creates gigantic opportunity for borrows under federally-backed and owned mortgages.

- PA Appellate Courts Schedule Arguments Using Electronic Media

- US Supreme Court holds that juries must render unanimous decisions in state criminal cases

- Signs of the Times — the future shortage of dentists.

{kind=link}